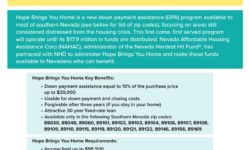

Up to $20,000 down payment Assistance

Own the home you always wanted New Government Program Makes it Easier than ever to own your Dream Home Call Now to Find out more 702-274-6006 Receive up to $20,000 in down payment assistance , let me help you maximize the assistance you qualify for